by Jeremy Hutton, policy analyst at the TaxPayers' Alliance

Executive summary

In the past, increases in the public debt were driven by major historical events, usually wars.

In the 18th century, a cycle of warfare saw British debt grow to unprecedented levels. These high levels of debt were tackled with urgency, but before each new war public debt would only be reduced to levels higher than those previously.

In contrast, the 19th century was peaceful. And despite an increasing level of financial crises as the economy industrialised, public debt was almost consistently reduced throughout the century.

Two world wars and two depressions would see public debt rise to its highest ever levels in the 20th century. It would take the UK 42 years to again reduce debt levels to those from the beginning of the century.

Now, the coronavirus crisis is seeing debt grow at its swiftest level since 2007-08, roughly comparable to the debt increases from 1939 to 1942 as a proportion of GDP. If the UK is to reduce it at the same pace as following the second world war, as a proportion of GDP, it would need to fall by 5.3 per cent annually for 8 years. But according to the government’s March budget, that won’t be happening anytime soon.

Introduction

The UK and many other countries around the world are inducing an unprecedented self-imposed recession to save lives from covid-19. To mitigate the length of this recession, the government has committed to a range of extraordinary measures to ensure that Britain can get back on its feet as soon as the pandemic passes.

These measures are set to be very costly, albeit understandable and justifiable. Ministers have announced numerous ways of raising the funds, such as gilt sales and quantitative easing, but how they will pay it back is another question. We can be confident that the UK public debt is set to rise.

Governments can use debt for a variety of reasons, such as to invest in the construction of key infrastructure. When interest rates are low, the costs of servicing the debt are more manageable. It can be a popular move because it mitigates the need for tax rises or service restrictions elsewhere, but it also shifts the burden onto future taxpayers. When governments maintain a reasonable level of public debt, the risks can be relatively low.

However, there are numerous issues with maintaining high levels of debt. First of all, higher debt levels mean more interest to pay. Secondly, if public spending is financed by debt in normal times, this reduces the fiscal headroom for responding to genuine national emergencies (like this one).

The current coronavirus emergency has invited frequent historical comparisons. But how apt are these comparisons, and how has Britain borrowed its way through the world-changing events of the past? Thankfully, the Bank of England has a treasure trove of valuable data to help us answer this question.

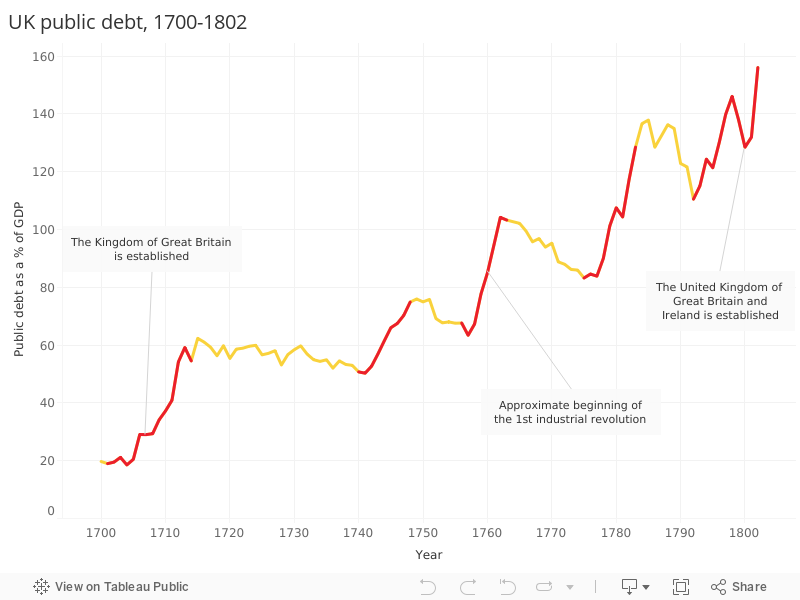

The 18th century

The 18th century was momentous for Britain, but it was also a period of conflict, as Britain and France engaged in more than a century of frequent warfare. As the chart above shows, each major conflict was associated with massive increases in the public debt, which was used to both finance significant military expansion and make up for the reduced revenues that resulted from interrupted trade flows.

It is notable that these increases in debt would never be entirely reduced prior to the next conflict, despite efforts to do so.

- 1701-1739: The war of the Spanish succession led to an ‘unprecedented’ debt burden. Despite the 25 years of relative peace prior to the next war, the government failed to reduce the debt.

- 1740-1748: Throughout the war of the Austrian succession, British national debt rose even further from 50.7 per cent of GDP to 74.9 per cent.

- 1749-1763: Although the national debt had been reduced to 67.7 per cent by the beginning of the seven years war, by the end of that war national debt would eclipse annual GDP for the first recorded time at 103 per cent.

- 1764-1774: The British government had no choice then but to address the national debt. As fighting in North America had been costly during the seven years war, the British government imposed new taxes there and tightened enforcement of some existing ones. This would contribute to the outbreak of the American war of independence in 1775.

- 1775-1783: Although by then the national debt was reduced to 83 per cent of GDP, in the ensuing war it would again reach new heights at 128.5 per cent of GDP.

- 1784-1791: Before the final war of the century, debt levels would fall by another 18 points to 110.5 per cent of GDP.

Despite the efforts to reduce the debt prior to each successive conflict after 1748, this cycle of conflicts took the national debt to previously unseen heights. Astonishingly, some debt of the period would not be paid off until 2015. Britain has never managed to return to the low debt levels prior to the war of the Spanish succession, although has twice got close: prior to the first world war in 1913 and at the end of Margaret Thatcher’s period as prime minister in 1990.

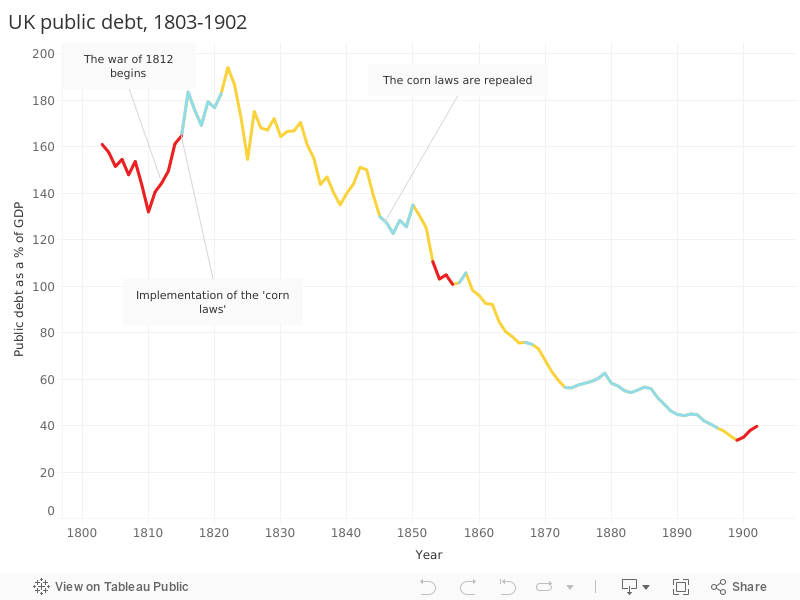

The 19th century

Beyond the defeat of Napoleon in 1815, the Crimean War in 1853, and frequent colonial wars, Britain enjoyed a largely peaceful 19th century with some very different challenges to overcome.

The birth of globalisation, long periods of peace and increasing industrialisation over the 19th century created an increasingly interconnected global economy, less reliant on agriculture for revenue. However, this also created an economy that became far more susceptible to wider-scale economic shocks. The ‘panic of 1825’ (referred to as the first modern financial crisis) happened as a result of widespread speculative investments into South America. In one notable example, a Scottish adventurer managed to convince many people to invest their savings into a fictional country called Poyais.

Britain would experience economic shocks more or less every decade of the 19th century, with some having very different effects to others. The terrible potato famine was the hallmark of the ‘hungry forties’, while the Long Depression bookended the UK’s century of great prosperity.

Overall, however, these recessions and occasional conflicts seem to have had only a minor effect upon public borrowing, easily offset in relatively short time as debt continuously declined throughout the century.

The period with the longest consistent decrease was from 1885 to 1899, during which Britain maintained a substantial primary surplus during the premierships of the Conservative Marquess of Salisbury and the Liberal William Gladstone.

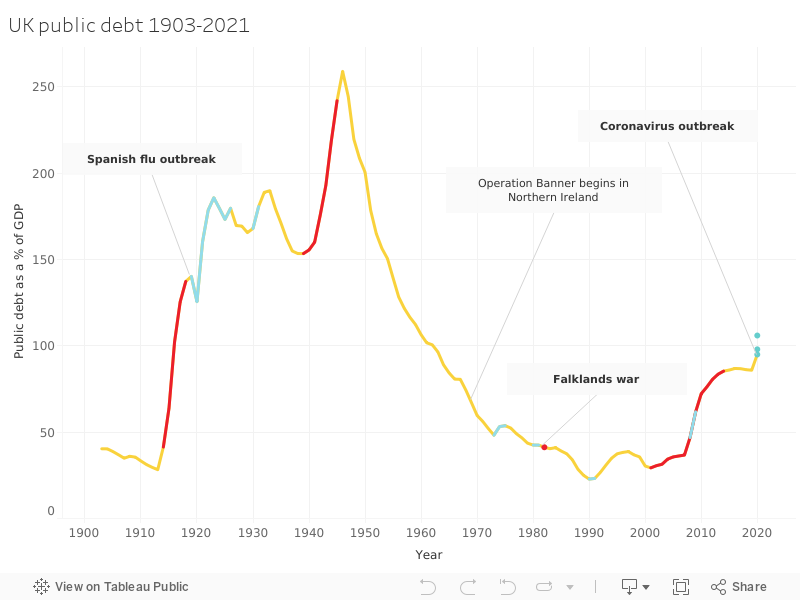

20th century onwards

The crises of the 20th century would take public debt to levels that would be considered shocking even by the standards of the early 19th century. The same level of debt that took 116 years to accumulate from 1706 to 1822 - and then took 91 years to reduce - took just 20 years to be rebuilt between the first world war and the great depression. It would be increased further to 259 per cent of GDP in the aftermath of the second world war.

The differences in the debt increases between the first and second world wars are particularly notable. From 1914 to 1915, for example, public debt as a proportion of GDP increased by 22 points. It would not be until four years into the second world war, 1943, that debt would have increased by the same proportion.

At the start of the second world war, the UK was unable to take out much needed US dollar loans due to a 1934 default on first world war American loans, right up until the beginning of ‘lend-lease’ in 1941. This remains a pertinent example of a past debt creating difficulties in a future crisis.

For the next forty years, Britain reduced the debt considerably. There is a notable uptick in the debt just prior to 1976, when James Callaghan took what was, at that point, the largest loan ever borrowed from the International Monetary Fund.

Although the wars in Afghanistan and Iraq did have an impact on the public finances and coincided with a period of increased borrowing, this is mostly coincidental, with that borrowing primarily driven by the financial crisis in 2008.

Coronavirus crisis

Since 1990, debt has consistently been rising and the current crisis will send it higher still. Where the 2008 crisis is notably different to those of the past (apart from the wars of the Spanish and Austrian successions in the 18th century) is that British debt has usually occurred in reverse V shapes. It rises dramatically as a result of the crisis, but then is reduced with relative speed. In recent times this has ceased to be the case, which casts doubt on the UK’s ability to reduce its currently increasing debt.

The Office for Budgetary Responsibility's (OBR) recent ‘reference scenario’ predicted that public debt would exceed 100 per cent of GDP during 2020-21, but by the year’s end would settle at 95 per cent of GDP and decline from there. Fitch, a global ratings agency, made a similar forecast but predicted debt would rise further to 98 per cent in 2020-21. Such levels of debt have not been seen since the 1960s.

In the OBR’s scenario, they predicted the current crisis would lead to increased borrowing of £218 billion this year. Notwithstanding any changes in interest rates or the specific manner by which the government raises the debt, interest payments on this could be £5.9 billion* on top of all other government debt interest.

The Resolution Foundation has predicted debt could reach 106 per cent of GDP this year, with forecasts for six and 12 month scenarios of 129 and 167 per cent of GDP respectively. The latter would place UK debt higher than it was at the end of the 18th century of warfare.

Historically, debt reduction occurred quicker than in the aftermath of the 2008 financial crisis. For example, between 1939 and 1942, debt had risen by 14.5 per cent. From 1946, it took 8 years to reduce debt to levels seen in 1939, meaning debt fell 42 per cent from its post-war peak. But current OBR estimates suggest that there will be a 16.7 per cent increase in debt in 2019-20, 22.2 per cent increase this year and 25 per cent next year (relative to their March budget forecasts). If the UK is to reduce it at the same pace as following the second world war, as a proportion of GDP, it would need to fall by 5.3 per cent annually for 8 years. Under current government plans, this is unlikely.

The Spanish flu also coincided with a very steep recession in the UK, with GDP falling dramatically between 1919 and 1921. During that time, debt was relatively stable, with the total debt stock barely changing. While it is difficult to make a straight comparison, it is nevertheless instructive that times of crises can see wildly different changes to total UK debt levels.

Conclusion

The past 15 years’ failure to reduce public debt cannot go on after the current coronavirus crisis. As we said in our statement on the coronavirus response, significant fiscal repair will be needed in the years afterwards. The scale of the challenge has illustrated the need for governments to be ready to take drastic action when required, underlining the importance of sound public finances in normal times. Debt levels will need to be brought back down rapidly through growth-enhancing measures and spending restraint. Supply-side repairs will be critical. We will need to be ready in case some other crisis happens.

Britain’s history shows that governments have almost always tried to reduce public debt after it increases to high levels. It may not have been completely reduced before the next crisis, but the debt is generally reduced by a significant margin. Recent governments would struggle to say they accomplished that.

Footnotes

*This estimate is based upon an effective interest rate on public sector borrowing of 2.7 per cent (not rounded for the calculation) for 2020-21 as forecast by the OBR in March 2020.

References - unless otherwise embedded

Carlos et al, The Origins of National Debt: The Financing and Re-financing of the War of the Spanish Succession, 2006.

Hancock, W, K, and Gowing, M, M., British War Economy, His Majesty’s Stationery Service, 1949.

Hills, S, and Thomas R., The UK recession in context — what do three centuries of data tell us? Bank of England, 2010.

Todman, D., Britain's War: Into Battle, 1937-1941, Penguin, 2016.